Confidence intervals for the extremal index \(\theta\) for "spm" objects

Source: R/confidence_intervals.R

spm_confint.Rdconfint method for objects of class c("spm", "exdex").

Computes confidence intervals for \(\theta\) based on an object returned

from spm. Two types of interval may be returned:

(a) intervals that are based on approximate large-sample normality of the

estimators of \(\theta\) (or of \(\log\theta\) if

conf_scale = "log"), and which are symmetric about the respective

point estimates, and (b) likelihood-based intervals based on an adjustment

of a naive (pseudo-) loglikelihood, using the

adjust_loglik function in the

chandwich package. The plot method plots the

log-likelihood for \(\theta\), with the required confidence interval(s)

indicated on the plot.

Usage

# S3 method for class 'spm'

confint(

object,

parm = "theta",

level = 0.95,

maxima = c("sliding", "disjoint"),

interval_type = c("norm", "lik", "both"),

conf_scale = c("theta", "log"),

constrain = TRUE,

bias_adjust = TRUE,

type = c("vertical", "cholesky", "spectral", "none"),

...

)

# S3 method for class 'confint_spm'

plot(x, estimator = "all", ndec = 2, ...)

# S3 method for class 'confint_spm'

print(x, ...)Arguments

- object

An object of class

c("spm", "exdex"), returned byspm.- parm

Specifies which parameter is to be given a confidence interval. Here there is only one option: the extremal index \(\theta\).

- level

A numeric scalar in (0, 1). The confidence level required.

- maxima

A character scalar specifying whether to estimate confidence intervals based on sliding maxima or disjoint maxima.

- interval_type

A character scalar:

"norm"for intervals of type (a),"lik"for intervals of type (b).- conf_scale

A character scalar. If

interval_type = "norm"thenconf_scaledetermines the scale on which we use approximate large-sample normality of the estimators to estimate confidence intervals of type (a).If

conf_scale = "theta"then confidence intervals are estimated for \(\theta\) directly. Ifconf_scale = "log"then confidence intervals are first estimated for \(\log\theta\) and then transformed back to the \(\theta\)-scale.Any bias-adjustment requested in the original call to

spm, using it'sbias_adjustargument, is automatically applied here.- constrain

A logical scalar. If

constrain = TRUEthen any confidence limits that are greater than 1 are set to 1, that is, they are constrained to lie in (0, 1]. Otherwise, limits that are greater than 1 may be obtained. Ifconstrain = TRUEthen any lower confidence limits that are less than 0 are set to 0.- bias_adjust

A logical scalar. If

bias_adjust = TRUEthen, if appropriate, bias-adjustment is also applied to the loglikelihood before it is adjusted usingadjust_loglik. This is performed only if, in the call tospm,bias_adjust = "BB3"or"BB1"was specified, that is, we haveobject$bias_adjust = "BB3"or"BB1". In these cases the relevant component ofobject$bias_slorobject$bias_djis used to scale \(\theta\) so that the location of the maximum of the loglikelihood lies at the bias-adjusted estimate of \(\theta\).If

bias_adjust = FALSEorobject$bias_adjust = "none"or"N"then no bias-adjustment of the intervals is performed. In the latter case this is because the bias-adjustment is applied in the creation of the data inobject$N2015_dataandobject$BB2018_data, on which the naive likelihood is based.- type

A character scalar. The argument

typeto be passed toconf_intervalsin thechandwichpackage in order to estimate the likelihood-based intervals. Usingtype = "none"is not advised because then the intervals are based on naive estimated standard errors. In particular, if (the default)sliding = TRUEwas used in the call tospmthen the unadjusted likelihood-based confidence intervals provide vast underestimates of uncertainty.- ...

Additional optional arguments to be passed to

print.default- x

an object of class

c("confint_spm", "exdex"), a result of a call toconfint.spm.- estimator

A character vector specifying which of the three variants of the semiparametric maxima estimator to include in the plot:

"N2015", "BB2018"or"BB2018b". Seespmfor details. Ifestimator = "all"then all three are included.- ndec

An integer scalar. The legend (if included on the plot) contains the confidence limits rounded to

ndecdecimal places.

Value

A list of class c("confint_spm", "exdex") containing the following components.

- cis

A matrix with columns giving the lower and upper confidence limits. These are labelled as (1 - level)/2 and 1 - (1 - level)/2 in % (by default 2.5% and 97.5%). The row names are a concatenation of the variant of the estimator (

N2015for Northrop (2015),BB2018for Berghaus and Bucher (2018)),BB2018bfor the modified (by subtracting1 / b) Berghaus and Bucher (2018) and the type of interval (normfor symmetric andlikfor likelihood-based).- ciN

The object returned from

conf_intervalsthat contains information about the adjusted loglikelihood for the Northrop (2015) variant of the estimator.- ciBB

The object returned from

conf_intervalsthat contains information about the adjusted loglikelihood for the Berghaus and Bucher (2018) variant of the estimator.- ciBBb

The object returned from

conf_intervalsthat contains information about the adjusted loglikelihood for the modified Berghaus and Bucher (2018) variant of the estimator.- call

The call to

spm.- object

The input

object.- maxima

The input

maxima.- theta

The relevant estimates of \(\theta\) returned from

adjust_loglik. These are equal toobject$theta_slifmaxima = "sliding",object$theta_djifmaxima = "disjoint", which provides a check that the results are correct.- level

The input

level.

plot.confint_spm: nothing is returned.

print.confint_spm: the argument x, invisibly.

Details

The likelihood-based intervals are estimated using the

adjust_loglik function in the

chandwich package, followed by a call to

conf_intervals.

This adjusts the naive (pseudo-)loglikelihood so that the curvature of

the adjust loglikelihood agrees with the estimated standard errors of

the estimators. The option type = "none" should not be used in

practice because the resulting confidence intervals will be wrong.

In particular, in the intervals based on sliding maxima will provide

vast underestimates of uncertainty.

If object$se contains NAs, because the block size b

was too small or too large in the call to spm then

confidence intervals cannot be estimated. A matrix of NAs

will be returned. See the Details section of the

spm documentation for more information.

print.confint_spm prints the matrix of confidence

intervals for \(\theta\).

References

Northrop, P. J. (2015) An efficient semiparametric maxima estimator of the extremal index. Extremes 18(4), 585-603. doi:10.1007/s10687-015-0221-5

Berghaus, B., Bucher, A. (2018) Weak convergence of a pseudo maximum likelihood estimator for the extremal index. Ann. Statist. 46(5), 2307-2335. doi:10.1214/17-AOS1621

See also

spm for estimation of the extremal index

\(\theta\) using a semiparametric maxima method.

Examples

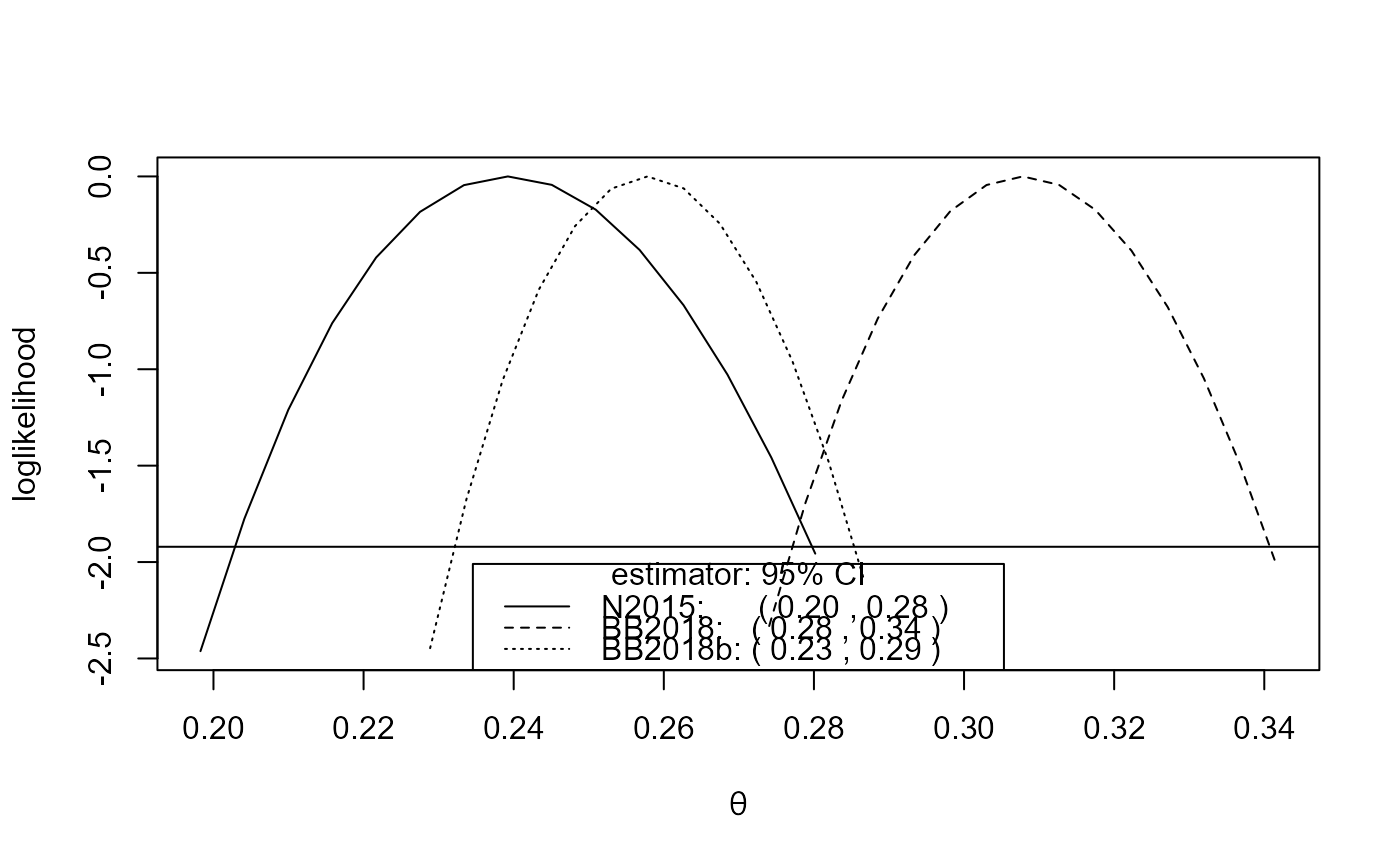

# Newlyn sea surges

theta <- spm(newlyn, 20)

confint(theta)

#> 2.5 % 97.5 %

#> N2015norm 0.2002191 0.2782277

#> BB2018norm 0.2756477 0.3399961

#> BB2018bnorm 0.2256477 0.2899961

cis <- confint(theta, interval_type = "lik")

cis

#> 2.5 % 97.5 %

#> N2015lik 0.2028802 0.2797593

#> BB2018lik 0.2771474 0.3407445

#> BB2018blik 0.2321583 0.2853566

plot(cis)

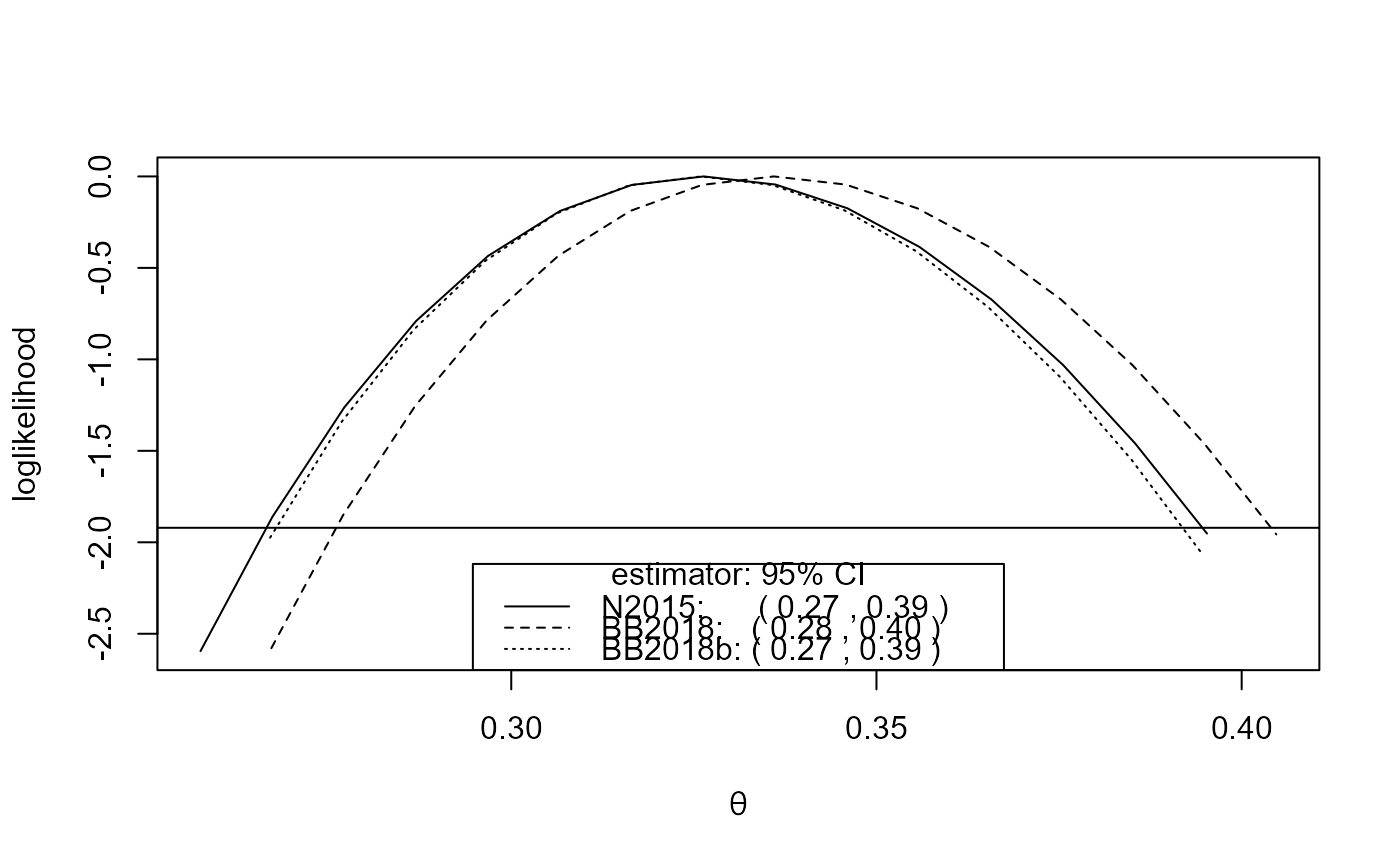

# S&P 500 index

theta <- spm(sp500, 100)

confint(theta)

#> 2.5 % 97.5 %

#> N2015norm 0.2607322 0.3919727

#> BB2018norm 0.2704307 0.4014686

#> BB2018bnorm 0.2604307 0.3914686

cis <- confint(theta, interval_type = "lik")

cis

#> 2.5 % 97.5 %

#> N2015lik 0.2664968 0.3946247

#> BB2018lik 0.2760426 0.4040249

#> BB2018blik 0.2678191 0.3919123

plot(cis)

# S&P 500 index

theta <- spm(sp500, 100)

confint(theta)

#> 2.5 % 97.5 %

#> N2015norm 0.2607322 0.3919727

#> BB2018norm 0.2704307 0.4014686

#> BB2018bnorm 0.2604307 0.3914686

cis <- confint(theta, interval_type = "lik")

cis

#> 2.5 % 97.5 %

#> N2015lik 0.2664968 0.3946247

#> BB2018lik 0.2760426 0.4040249

#> BB2018blik 0.2678191 0.3919123

plot(cis)