Chapter 10: Correlation

Paul Northrop

Source:vignettes/stat0002-ch9plus1-correlation-vignette.Rmd

stat0002-ch9plus1-correlation-vignette.RmdThis vignette provides some R code that is related to some of the content of Chapter 10 of the STAT0002 notes correlation.

Example data

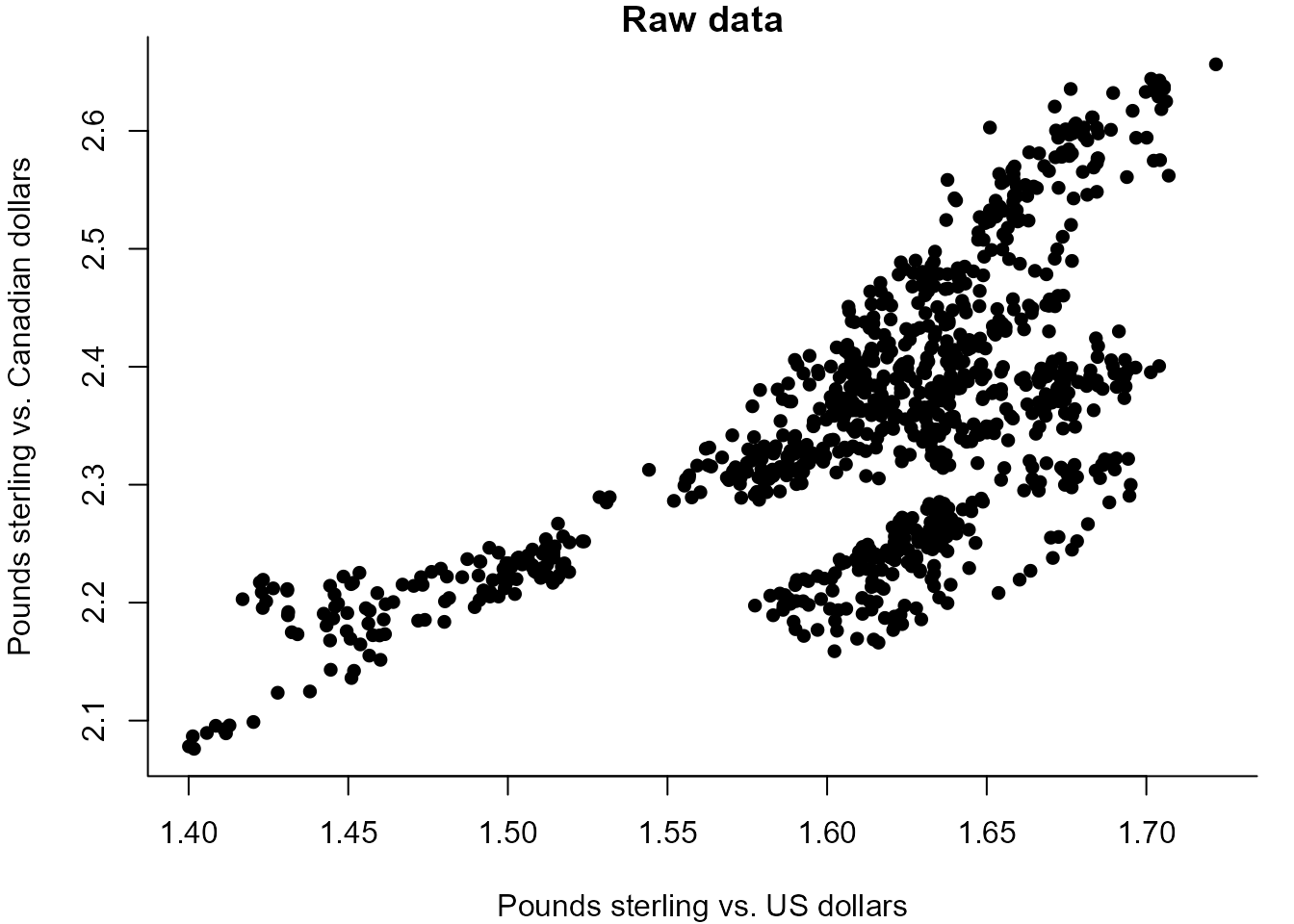

We use the exchange rate data described at the start of Section

10.1 of the notes. These data are available in the data frame

exchange. We look at the first 6 rows of the data and the

last 6 rows and produce plots like Figures 10.1 and 10.2 of the

notes.

> head(exchange)

USD.GBP CAD.GBP

1997/01/02 1.6865 2.3167

1997/01/03 1.6905 2.3224

1997/01/06 1.6855 2.3056

1997/01/07 1.6951 2.2999

1997/01/08 1.6884 2.2850

1997/01/09 1.6947 2.2906

> tail(exchange)

USD.GBP CAD.GBP

2000/11/14 1.4309 2.2102

2000/11/15 1.4265 2.2121

2000/11/16 1.4229 2.2088

2000/11/17 1.4233 2.2194

2000/11/20 1.4223 2.2172

2000/11/21 1.4169 2.2029

> # Figure 10.1

> plot(exchange, pch = 16, xlab = "Pounds sterling vs. US dollars",

+ ylab = "Pounds sterling vs. Canadian dollars", bty = "l",

+ main = "Raw data")

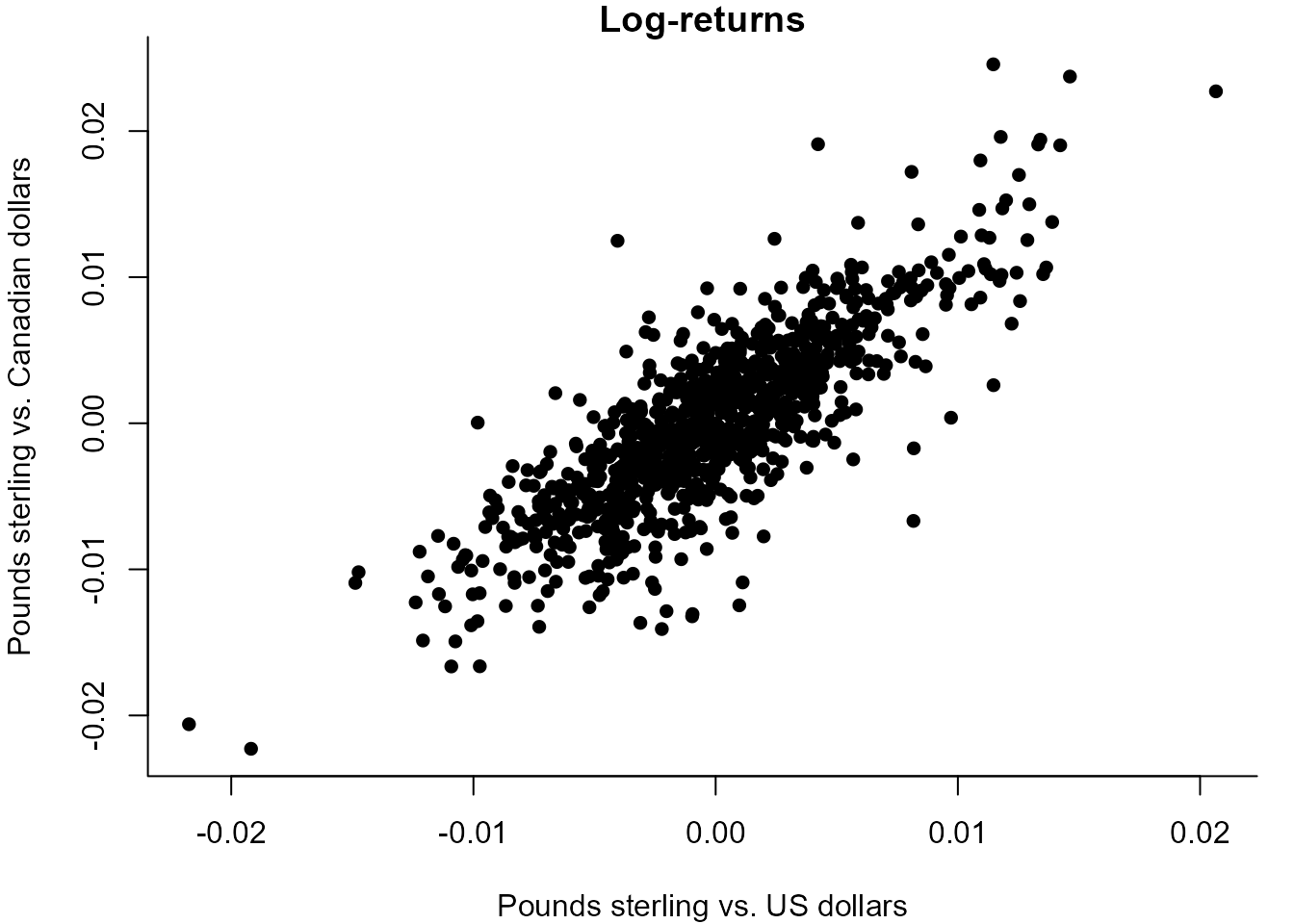

> # Calculate the log-returns

> USDlogr <- diff(log(exchange$USD.GBP))

> CADlogr <- diff(log(exchange$CAD.GBP))

> # Figure 10.2

> plot(USDlogr, CADlogr, pch = 16, xlab = "Pounds sterling vs. US dollars",

+ ylab = "Pounds sterling vs. Canadian dollars", bty = "l",

+ main = "Log-returns" )

The R function cor

R provides a function cor to calculate sample

correlation coefficients. By default, it calculates the sample (product

moment) correlation coefficient given in Section

10.2.1.

We can supply either two vectors x and y of

equal length or a matrix with columns containing the vectors of data for

which we want to calculate the sample correlation coefficient. In this

case, we create a 2-column matrix using cbind function to

combine the 2 vectors USDlogr and CADlogr

columnwise into a matrix.

If we supply a matrix then R will return a matrix containing the

sample correlation coefficients between all possible pairs of columns in

the input matrix, including between each column and itself, which

produces values of 1 on the diagonal of the output matrix. If we supply

vectors x and y then it does not matter which

vector is entered as x and which as y.

Anscombe’s Quartet of datasets

In Section

10.3.6 Anscombe’s Quartet of dataset are provided in Figure 10.9.

These 4 datasets are available as separate data frames in the

anscombiser package Northrop

(2022). Use install.packages("anscombiser") to

install this package.

> cor(anscombe1)

x1 y1

x1 1.0000000 0.8164205

y1 0.8164205 1.0000000

> cor(anscombe2)

x2 y2

x2 1.0000000 0.8162365

y2 0.8162365 1.0000000

> cor(anscombe3)

x3 y3

x3 1.0000000 0.8162867

y3 0.8162867 1.0000000

> cor(anscombe4)

x4 y4

x4 1.0000000 0.8165214

y4 0.8165214 1.0000000We see that the paired data in these datasets have almost exactly the same sample correlation coefficient. They have many other summary statistics in common. See Section 10.3.6 for details.

The method argument to cor enables us to

ask R to calculate Spearman’s rank correlation coefficient (See Section

2.3.5). The values of this sample correlation coefficient differ

between these datasets.

> cor(anscombe1, method = "spearman")

x1 y1

x1 1.0000000 0.8181818

y1 0.8181818 1.0000000

> cor(anscombe2, method = "spearman")

x2 y2

x2 1.0000000 0.6909091

y2 0.6909091 1.0000000

> cor(anscombe3, method = "spearman")

x3 y3

x3 1.0000000 0.9909091

y3 0.9909091 1.0000000

> cor(anscombe4, method = "spearman")

x4 y4

x4 1.0 0.5

y4 0.5 1.0